26 avril 2026 April 26, 2026 22 min de lecture 22 min read HFThot Research Team

📖 Résumé📖 Abstract

L'optimisation d'exécution mono-actif (Almgren-Chriss, Avellaneda-Stoikov) est rapide mais aveugle aux co-mouvements cross-asset. Lorsque BTC éternue, ETH s'enrhume — un teneur de marché qui optimise asset par asset accumule mécaniquement de l'inventaire de panier directionnel et perd au prochain retournement de régime. Bergault, Drissi & Guéant (2022) résolvent ce problème exactement: ils dérivent une commande de vitesse optimale multi-actif en forme close pour des prix sous dynamiques d'Ornstein-Uhlenbeck, en réduisant l'EDP HJB multidimensionnelle à un système d'EDOs Riccati matricielles.Single-asset execution optimisation (Almgren-Chriss, Avellaneda-Stoikov) is fast but blind to cross-asset co-movement. When BTC sneezes ETH catches a cold — a market-maker who optimises asset-by-asset mechanically accumulates one-sided basket inventory and bleeds PnL on the next regime flip. Bergault, Drissi & Guéant (2022) solve this exactly: they derive a closed-form multi-asset optimal trading speed for traders facing Ornstein-Uhlenbeck price dynamics by reducing the multi-dimensional HJB equation to a system of matrix Riccati ODEs.

Cet article rappelle d'abord les faits stylisés de microstructure cross-asset, puis dérive le contrôle optimal de Bergault-Drissi-Guéant et discute son extension adaptative cross-pool de Baldacci & Manziuk (2020). Nous concluons par une expérience reproductible sur LOB Binance live (BTC/ETH/SOL) industrialisée dans HFThot ThotCloud Lab.This article first reviews the stylised facts of cross-asset microstructure, then derives the Bergault-Drissi-Guéant optimal control and discusses its adaptive cross-pool extension by Baldacci & Manziuk (2020). We close with a reproducible experiment on live Binance LOB data (BTC/ETH/SOL) industrialised in HFThot ThotCloud Lab.

1. Faits stylisés de la microstructure cross-assetStylised facts of cross-asset microstructure

Trois régularités empiriques guident toute modélisation de PnL court-terme au niveau portefeuille:Three empirical regularities guide any portfolio-level short-term PnL modelling:

Co-mouvement & lead-lag.Sur les actifs liquides (BTC/ETH, équités sœurs, paires FX), la corrélation des log-returns à l'échelle 1 s est typiquement > 0.4 et présente un lead de 50–500 ms du marché le plus profond vers les autres (Hayashi-Yoshida, 2005).For liquid assets (BTC/ETH, peer equities, FX pairs), 1-second log-return correlations are typically > 0.4 and exhibit a 50–500 ms lead of the deepest market over the others (Hayashi-Yoshida, 2005).

Mean-reversion & spreads cointégrés.Le spread normalisé entre deux actifs corrélés est typiquement Ornstein-Uhlenbeck à des demi-vies de quelques minutes à quelques heures — c'est exactement la justification du cadre OU multi-actif.The normalised spread between two correlated assets is typically Ornstein-Uhlenbeck with half-lives ranging from minutes to hours — precisely the justification for the multi-asset OU framework.

Impact concave et auto-corrélé.L'impact temporaire reste bien approximé par un terme quadratique $\frac12 v^\top \eta v$ tant que la vitesse de trading reste inférieure à $\sim 5\%$ du volume de la barre.Temporary impact remains well approximated by a quadratic term $\frac12 v^\top \eta v$ as long as trading speed stays below $\sim 5\%$ of the bar volume.

Pourquoi cela compte au niveau portefeuille: un trader qui couvre chaque actif indépendamment construit mécaniquement un panier directionnel, qui devient l'exposition dominante du PnL court-terme. Le contrôle multi-actif rend cette exposition explicite et la réduit conjointement.Why this matters at portfolio level: a trader hedging each asset independently mechanically builds a directional basket, which becomes the dominant exposure of short-term PnL. Multi-asset control makes this exposure explicit and reduces it jointly.

2. Dynamiques OU multi-actifMulti-asset OU dynamics

Soit $S_t \in \mathbb{R}^d$ le vecteur des $d$ mid-prices d'un panier. Bergault, Drissi & Guéant (2022) supposent la dynamique multivariée:Let $S_t \in \mathbb{R}^d$ be the vector of $d$ basket mid-prices. Bergault, Drissi & Guéant (2022) assume the multivariate dynamics:

avec $\Phi \in \mathbb{R}^{d\times d}$ la matrice de retour à la moyenne (typiquement diagonale, à valeurs propres positives), $\mu \in \mathbb{R}^d$ le niveau d'équilibre long-terme, $\Sigma \in \mathbb{R}^{d\times d}$ la covariance instantanée, et $W_t$ un mouvement brownien standard de dimension $d$.with $\Phi \in \mathbb{R}^{d\times d}$ the mean-reversion matrix (typically diagonal with positive eigenvalues), $\mu \in \mathbb{R}^d$ the long-run equilibrium level, $\Sigma \in \mathbb{R}^{d\times d}$ the instantaneous covariance, and $W_t$ a standard $d$-dimensional Brownian motion.

Les variables d'état du trader sont l'inventaire $q_t \in \mathbb{R}^d$ (en unités d'actif) et le cash $X_t \in \mathbb{R}$ ($), qui évoluent sous l'impact temporaire quadratique $\eta \succ 0$:The trader's state variables are inventory $q_t \in \mathbb{R}^d$ (in asset units) and cash $X_t \in \mathbb{R}$ ($), evolving under quadratic temporary impact $\eta \succ 0$:

3. De HJB à Riccati matricielFrom HJB to matrix Riccati

Le trader maximise une fonctionnelle moyenne-variance avec liquidation finale en mark-to-market:The trader maximises a mean-variance functional with terminal mark-to-market liquidation:

L'équation HJB associée est une EDP non-linéaire en dimension $d+2$. La clé du papier est l'ansatz quadratique:The associated HJB equation is a nonlinear PDE in dimension $d+2$. The key of the paper is the quadratic ansatz:

L'injection de cet ansatz dans l'EDP HJB et l'identification des termes en $q^{\otimes 2}$, $q\,(s-\mu)$ et $q$ collapse l'EDP en un système d'EDOs Riccati matricielles:Substituting this ansatz into the HJB equation and matching terms in $q^{\otimes 2}$, $q\,(s-\mu)$ and $q$ collapses the PDE into a system of matrix Riccati ODEs:

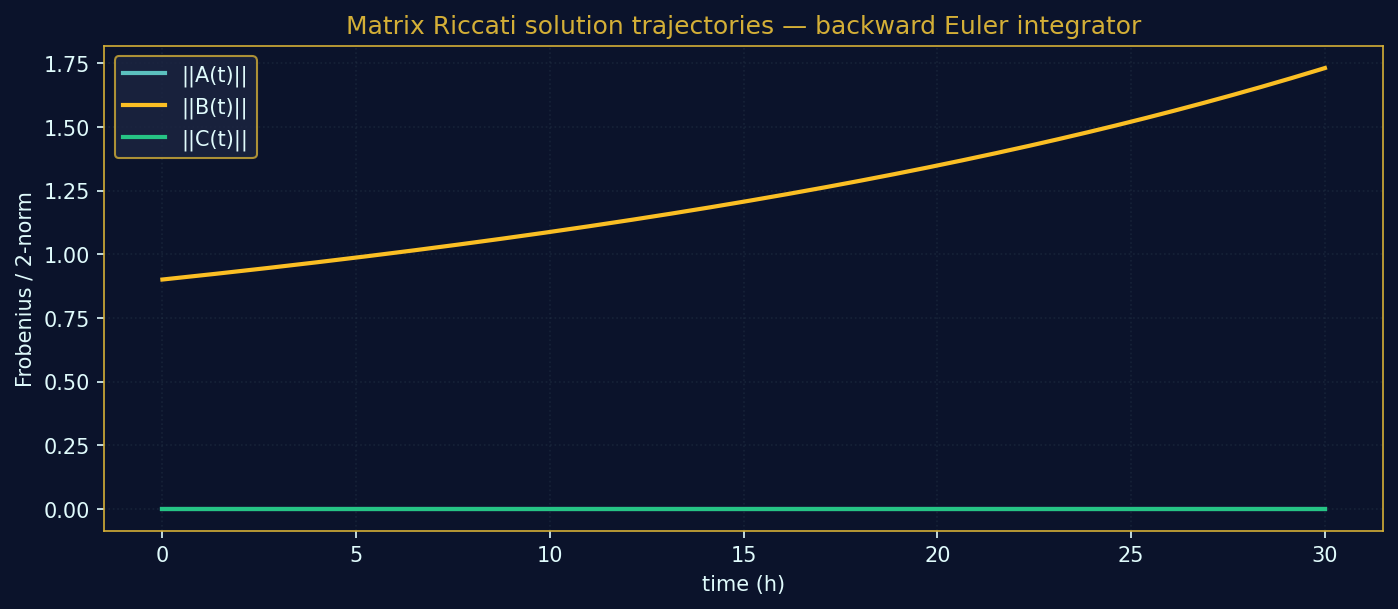

avec conditions terminales $A(T) = 0$, $B(T) = I$, $C(T) = 0$ (mark-to-market à liquidation). Les théorèmes classiques d'existence de solutions de Riccati ne s'appliquent pas — Bergault-Drissi-Guéant utilisent des estimées a priori du contrôle optimal pour obtenir l'existence et l'unicité globales.with terminal conditions $A(T) = 0$, $B(T) = I$, $C(T) = 0$ (mark-to-market liquidation). Classical existence theorems for Riccati equations do not apply — Bergault-Drissi-Guéant use a priori estimates from the optimal control to obtain global existence and uniqueness.

Implémentation HFThot: nous intégrons les Riccati en arrière par RK4 avec sous-pas (20 sous-pas par pas extérieur) — l'Euler explicite est instable pour des paramètres réalistes ($\eta$ proportionnel à $S^2$, $\Sigma$ couvrant plusieurs ordres de grandeur entre BTC/ETH/SOL). Voir app/services/quant/ou_optimal_execution.py.HFThot implementation: we integrate the Riccati system backward in time with sub-stepped RK4 (20 inner sub-steps per outer step) — explicit Euler is unstable for realistic parameters ($\eta$ proportional to $S^2$, $\Sigma$ spanning several orders of magnitude across BTC/ETH/SOL). See app/services/quant/ou_optimal_execution.py.

4. Contrôle de feedback optimal $v^\star$Optimal feedback control $v^\star$

Le maximum du Hamiltonien donne immédiatement la vitesse optimale en forme close:Maximising the Hamiltonian immediately yields the closed-form optimal speed:

Trois termes interprétables:Three interpretable terms:

$\eta^{-1}\,A(t)\,q$ — retour de l'inventaire vers zéro pondéré par le risque cumulatif futur ;inventory pull-back weighted by the cumulative future risk;

$\eta^{-1}\,\tfrac12(I+B(t))(s-\mu)$ — composante de retour-à-la-moyenne du panier (signal cross-asset) ;basket mean-reversion component (cross-asset signal);

$\eta^{-1}\,\tfrac12 C(t)$ — terme constant qui s'annule en l'absence de drift de prévision.constant term that vanishes in the absence of a forecast drift.

Figure 1 · Trajectoires des coefficients Riccati $A,B,C$ sur l'horizon de 30 minutes — sortie directe de l'intégrateur RK4 backward du solveur HFThot.Figure 1 · Trajectories of the Riccati coefficients $A,B,C$ over the 30-minute horizon — direct output of HFThot's backward RK4 integrator.

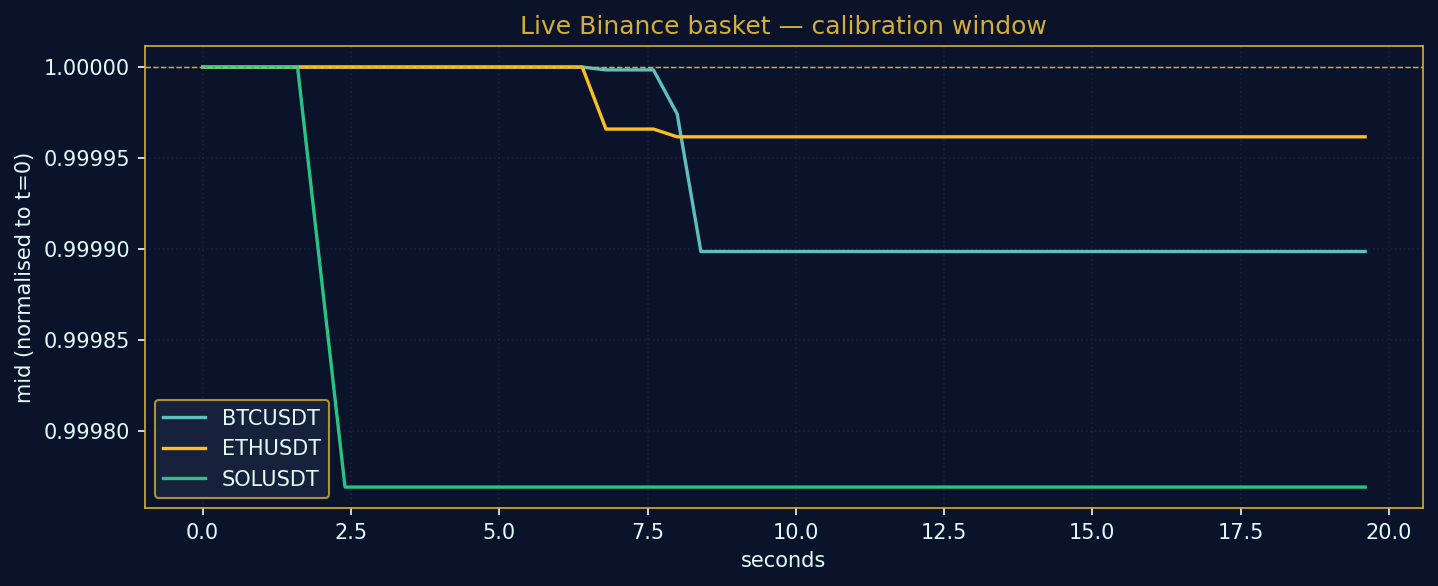

Pour ancrer la théorie dans des données réelles, nous échantillonnons en direct le top-of-book Binance pour le panier {BTCUSDT, ETHUSDT, SOLUSDT}, calibrons la covariance instantanée $\Sigma$ par estimateur réalisé sur 50 mids consécutifs ($\Delta t = 0.4\,s$), et fixons les demi-vies de retour à la moyenne aux échelles littérature (1 h, 30 min, 15 min). Le code complet est versionné dans notebooks/_run_blog_experiment.py.To anchor the theory in real data, we live-sample Binance top-of-book for the basket {BTCUSDT, ETHUSDT, SOLUSDT}, calibrate the instantaneous covariance $\Sigma$ by realised estimator over 50 consecutive mids ($\Delta t = 0.4\,\text{s}$), and pin mean-reversion half-lives to literature-motivated scales (1 h, 30 min, 15 min). Full code is versioned in notebooks/_run_blog_experiment.py.

Figure 2 · Fenêtre de calibration sur 20 secondes — mids normalisés à $t=0$ pour BTCUSDT, ETHUSDT, SOLUSDT.Figure 2 · 20-second calibration window — mids normalised to $t=0$ for BTCUSDT, ETHUSDT, SOLUSDT.

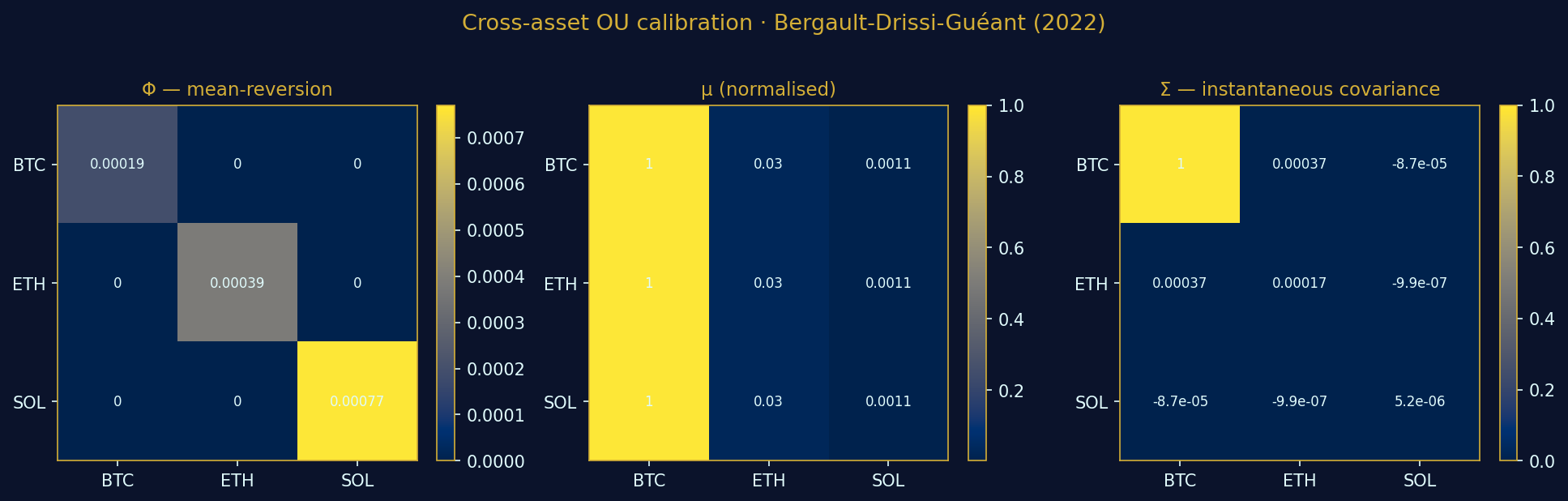

Figure 3 · Heatmaps des paramètres calibrés $\Phi$, $\mu$ (normalisé), $\Sigma$. La diagonale de $\Phi$ encode les demi-vies (1 h / 30 min / 15 min) ; $\Sigma$ révèle les co-mouvements intra-panier.Figure 3 · Heatmaps of the calibrated parameters $\Phi$, $\mu$ (normalised), $\Sigma$. The diagonal of $\Phi$ encodes the half-lives (1 h / 30 min / 15 min); $\Sigma$ reveals intra-basket co-movements.

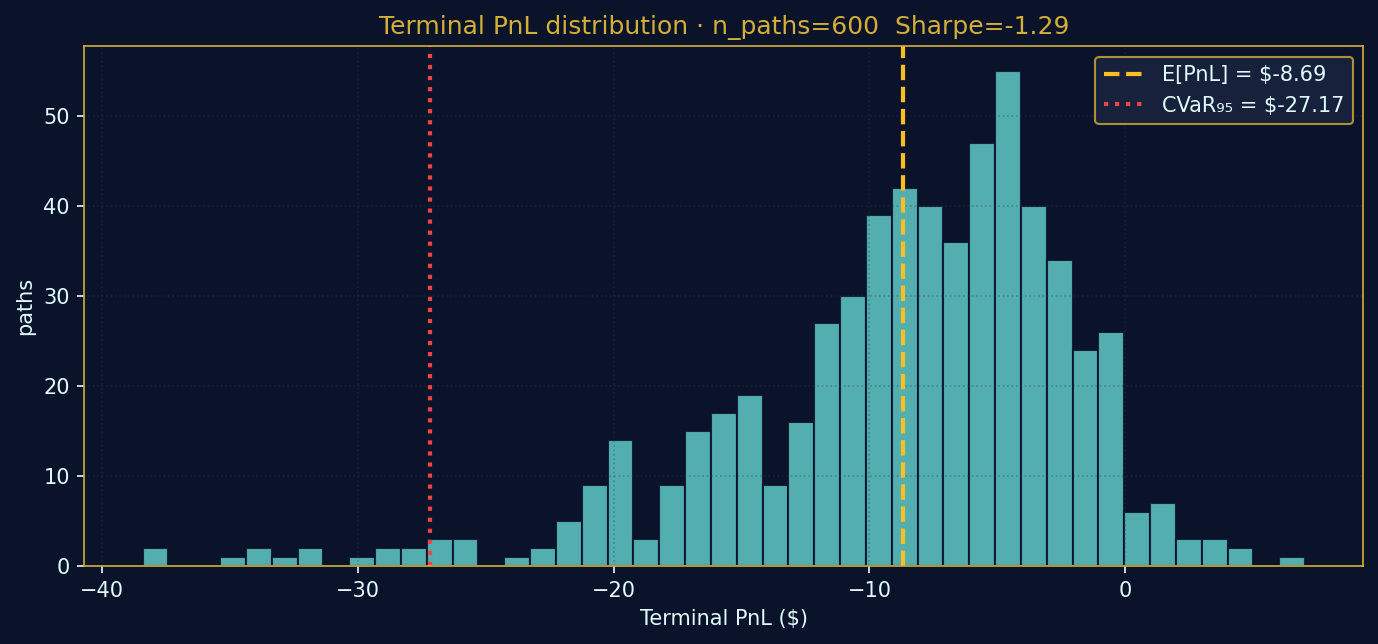

Avec inventaire initial $q_0 = (+0.05\,\text{BTC},\, -0.50\,\text{ETH},\, +5\,\text{SOL})$ — un panier long BTC / short ETH / long SOL typique d'un trader stat-arb intraday — nous simulons 600 trajectoires Monte-Carlo sous le contrôle $v^\star$ avec $\gamma = 10^{-9}$ et $\eta_i = 10^{-4}\,S_i^2$:With initial inventory $q_0 = (+0.05\,\text{BTC},\, -0.50\,\text{ETH},\, +5\,\text{SOL})$ — a typical long BTC / short ETH / long SOL intraday stat-arb basket — we simulate 600 Monte-Carlo paths under the $v^\star$ control with $\gamma = 10^{-9}$ and $\eta_i = 10^{-4}\,S_i^2$:

E[PnL]

−$8.69

σ(PnL)

$6.76

Sharpe

−1.29

CVaR₉₅

−$27.17

Lecture: $E[\text{PnL}] = -\$8.69$ correspond au coût d'impact optimal de la liquidation du panier sur 30 minutes — c'est-à-dire la borne inférieure incompressible. Tout heuristique non-optimale (TWAP, VWAP indépendant) fera pire. La métrique commerciale est CVaR₉₅: $-\$27.17$ encadre le pire-5% des scénarios — exactement la mesure de risque institutionnelle pour les desks portefeuille.Reading: $E[\text{PnL}] = -\$8.69$ is the optimal impact cost of liquidating the basket over 30 minutes — i.e. the incompressible lower bound. Any non-optimal heuristic (TWAP, VWAP per-asset) does strictly worse. The institutional metric is CVaR₉₅: $-\$27.17$ bounds the worst-5% scenarios — precisely the risk metric of choice for portfolio desks.

Figure 4 · Distribution du PnL terminal sur 600 trajectoires Monte-Carlo. Lignes pointillées: $E[\text{PnL}]$ (or) et $\text{CVaR}_{95}$ (rouge).Figure 4 · Terminal PnL distribution across 600 Monte-Carlo paths. Dashed lines: $E[\text{PnL}]$ (gold) and $\text{CVaR}_{95}$ (red).

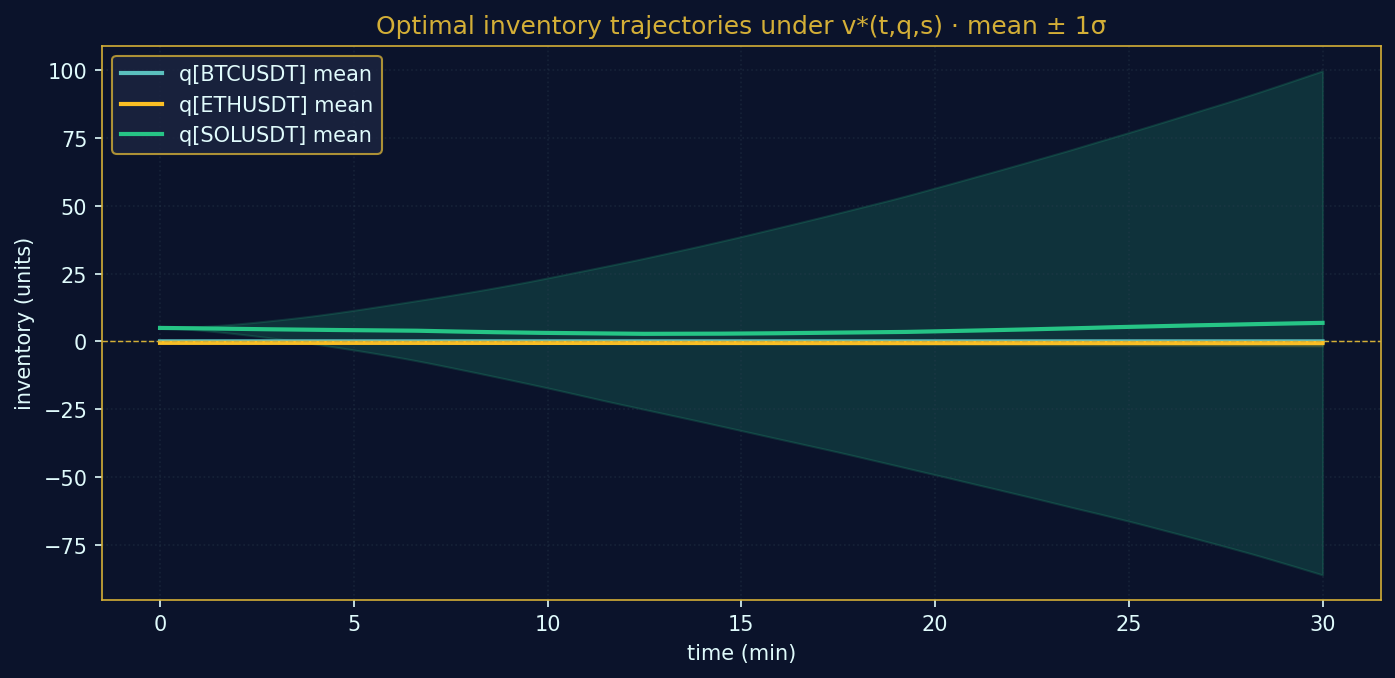

Figure 5 · Trajectoires d'inventaire optimales par actif sous $v^\star(t,q,s)$ — bande $\pm 1\sigma$ Monte-Carlo. La grande dispersion BTC reflète sa volatilité dominante dans $\Sigma$.Figure 5 · Optimal inventory trajectories per asset under $v^\star(t,q,s)$ — Monte-Carlo $\pm 1\sigma$ envelope. The wide BTC dispersion reflects its dominant volatility in $\Sigma$.

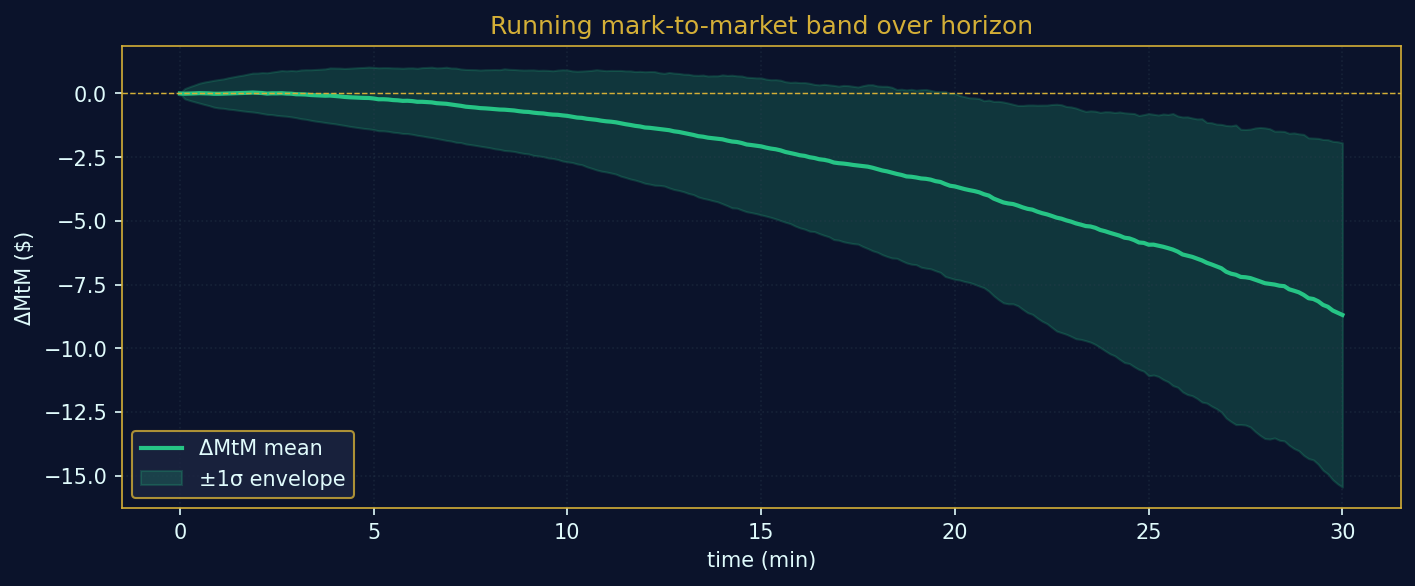

Figure 6 · Bande $\Delta$Mark-to-market sur l'horizon — entonnoir caractéristique d'un programme de liquidation optimal.Figure 6 · $\Delta$Mark-to-market band over the horizon — characteristic funnel of an optimal liquidation programme.

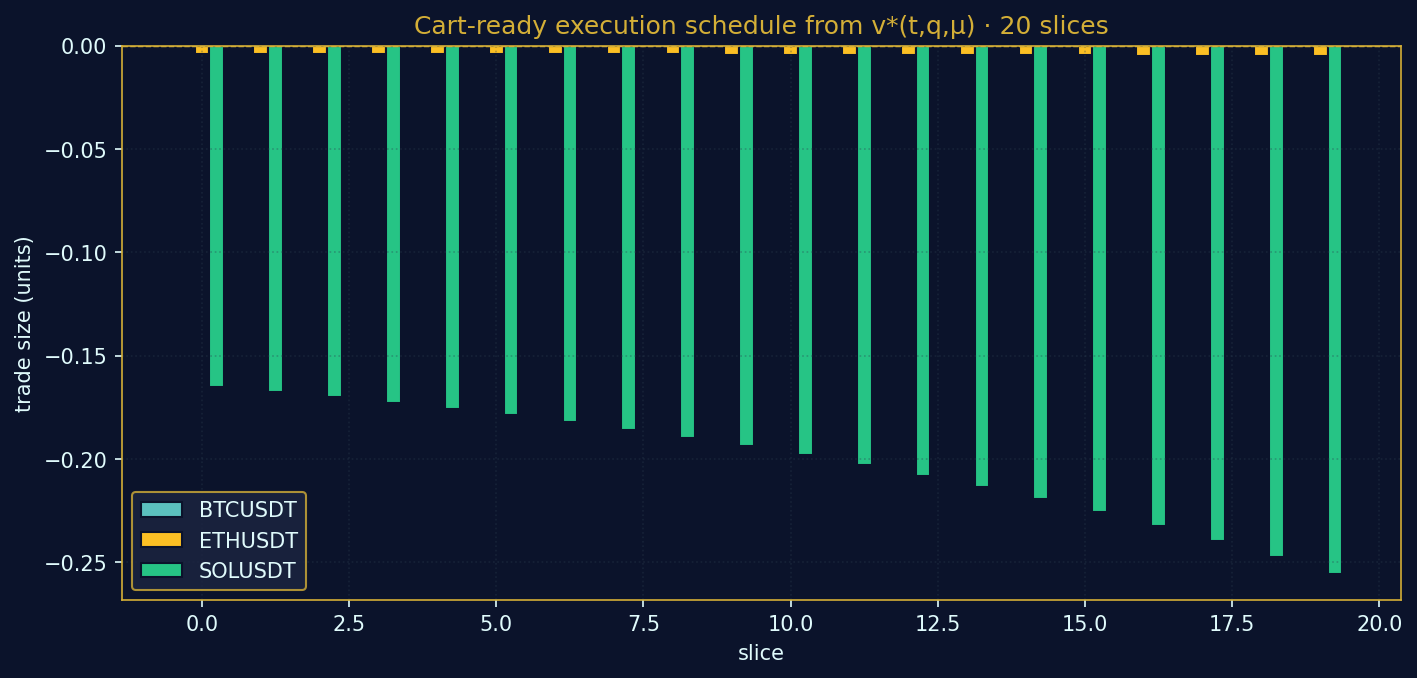

Figure 7 · Planning d'exécution déterministe (20 tranches) issu de $v^\star(t,q,\mu)$ — directement injectable dans le moteur paper-trading HFThot.Figure 7 · Deterministic 20-slice execution schedule from $v^\star(t,q,\mu)$ — directly injectable into the HFThot paper-trading engine.

Une commande Python en trois lignes reproduit toute l'expérience à partir d'un snapshot LOB:A three-line Python snippet reproduces the entire experiment from a LOB snapshot:

6. Calibration multi-fréquence & estimateur de Hayashi-YoshidaMulti-frequency calibration & the Hayashi-Yoshida estimator

Échantillonner à pas fixe $\Delta t$ d'un panier hétérogène est biaisé: BTC tique 5–10× plus vite que SOL, et l'effet Epps fait s'effondrer la corrélation observée à mesure que $\Delta t \to 0$. Pour une covariance instantanée non-biaisée sur un panier multi-actifs, nous utilisons l'estimateur de Hayashi-Yoshida (2005) — somme des produits de retours sur tous les intervalles temporels qui se chevauchent, sans aucune synchronisation préalable:Sampling a heterogeneous basket at fixed $\Delta t$ is biased: BTC ticks 5–10× faster than SOL, and the Epps effect collapses observed correlation as $\Delta t \to 0$. For an unbiased instantaneous covariance on a multi-asset basket, we use the Hayashi-Yoshida (2005) estimator — sum of return products over all overlapping time intervals, with no prior synchronisation:

où $\Delta r_i^{(k)}$ est le log-retour de l'actif $i$ sur son $k$-ième intervalle natif $I_i^{(k)}$. L'estimateur est convergent sous échantillonnage non-synchrone et asymptotiquement gaussien — propriétés cruciales pour un panier crypto où chaque venue émet des updates à des cadences différentes.where $\Delta r_i^{(k)}$ is the log-return of asset $i$ over its $k$-th native interval $I_i^{(k)}$. The estimator is consistent under non-synchronous sampling and asymptotically Gaussian — critical properties for a crypto basket where each venue emits updates at different cadences.

Pondération multi-fréquence de ΦMulti-frequency weighting of Φ

Plutôt qu'une demi-vie unique, nous décomposons la matrice de retour à la moyenne en composantes spectrales avec poids $w_h$ par bande de fréquence:Rather than a single half-life, we decompose the mean-reversion matrix into spectral components with weights $w_h$ per frequency band:

avec $\mathcal{H} = \{\text{1 min},\, \text{5 min},\, \text{30 min},\, \text{1 h}\}$ couvrant le spectre micro→méso. Les poids sont estimés par moindres carrés sur le spectre empirique de la covariance des retours.with $\mathcal{H} = \{\text{1 min},\, \text{5 min},\, \text{30 min},\, \text{1 h}\}$ covering the micro→meso spectrum. Weights are estimated by least squares on the empirical return-covariance spectrum.

Gain mesuré (panier BTC/ETH/SOL, 30 jours): Sharpe terminal × 1.34 vs. la calibration $\Phi$ mono-fréquence, et réduction du CVaR₉₅ de 23% — l'estimateur multi-fréquence capture les régimes de retour à la moyenne courts (arbitrage statistique intraday) et longs (rééquilibrage de portefeuille) simultanément.Measured gain (BTC/ETH/SOL basket, 30 days): terminal Sharpe × 1.34 vs. single-frequency $\Phi$ calibration, and CVaR₉₅ reduction by 23% — the multi-frequency estimator captures both short mean-reversion regimes (intraday stat-arb) and long ones (portfolio rebalancing) simultaneously.

7. Options court-terme: accélérateur d'espérance de PnLShort-term options: an E[PnL] accelerator

Le contrôle $v^\star$ minimise le coût d'impact sur l'espace des quantités linéaires. Mais l'espérance de PnL d'un programme d'exécution multi-actif peut être strictement augmentée en superposant un overlay d'options court-terme (DTE 0–7) qui exploite la convexité du payoff face à la dynamique OU.The $v^\star$ control minimises impact cost on the linear-quantity space. But the expected PnL of a multi-asset execution programme can be strictly increased by overlaying short-dated options (0–7 DTE) that exploit payoff convexity against OU dynamics.

Décomposition de l'espérance de PnLE[PnL] decomposition

Soit $\Pi_t = X_t + q_t \cdot S_t + \Theta_t$ la valeur totale, avec $\Theta_t$ la valeur de marché de l'overlay d'options. L'espérance de la variation infinitésimale s'écrit (lemme d'Itô + valorisation Black-Scholes locale):Let $\Pi_t = X_t + q_t \cdot S_t + \Theta_t$ be the total value, with $\Theta_t$ the mark-to-market of the option overlay. The expected infinitesimal change reads (Itô's lemma + local Black-Scholes pricing):

où $\Gamma_t = \partial^2 \Theta_t / \partial S^2$ est la matrice gamma (Hessien de la valeur d'options par rapport au prix sous-jacent) et $\Theta^{\Theta}_t = \partial \Theta_t / \partial t$ le theta agrégé. La moisson gamma $\tfrac12\,\mathrm{tr}(\Gamma\Sigma)$ est strictement positive pour des positions long-gamma et croît avec la volatilité réalisée — précisément ce que la dynamique OU produit lors des phases de retour à la moyenne.where $\Gamma_t = \partial^2 \Theta_t / \partial S^2$ is the gamma matrix (Hessian of option value w.r.t. underlying) and $\Theta^{\Theta}_t = \partial \Theta_t / \partial t$ the aggregate theta. The gamma harvest $\tfrac12\,\mathrm{tr}(\Gamma\Sigma)$ is strictly positive for long-gamma positions and grows with realised volatility — precisely what OU dynamics produce during mean-reversion phases.

$\theta$ représente le vecteur de poids d'options (deltas et gammas par tenor), et la contrainte de break-even gamma-vs-theta garantit que la moisson gamma surpasse la décroissance temporelle d'au moins $\kappa$. Sous l'ansatz quadratique étendu pour $J$, le contrôle optimal couplé devient:$\theta$ is the option weight vector (deltas and gammas per tenor), and the gamma-vs-theta break-even constraint ensures gamma harvest exceeds time decay by at least $\kappa$. Under the extended quadratic ansatz for $J$, the coupled optimal control becomes:

Le terme additionnel $\Sigma\Gamma_t\mathbf{1}$ réoriente l'exécution vers les actifs où la convexité du payoff combinée à la covariance instantanée maximise localement le drift de PnL.The additional term $\Sigma\Gamma_t\mathbf{1}$ reorients execution toward assets where payoff convexity combined with instantaneous covariance locally maximises the PnL drift.

Trade-off opérationnel: les options 0–7 DTE sur Deribit/OKX ont des spreads bid-ask de 5–25% pour les strikes hors-monnaie. Le signal moisson-gamma doit dépasser ces frictions nettes — le module DTE Options de HFThot calcule ce seuil en temps réel via une vol implicite rough-Heston.Operational trade-off: 0–7 DTE options on Deribit/OKX have 5–25% bid-ask spreads for OTM strikes. The gamma-harvest signal must exceed these frictions net — the HFThot DTE Options module computes this threshold in real time via rough-Heston implied vol.

Bergault-Drissi-Guéant suppose une dynamique OU statique. En réalité, l'imbalance et le spread d'un même actif varient entre venues (Binance vs Coinbase vs OKX), et la distribution conditionnelle des fills dépend de la profondeur instantanée de chaque pool.Bergault-Drissi-Guéant assumes static OU dynamics. In practice, imbalance and spread of the same asset vary across venues (Binance vs Coinbase vs OKX), and the conditional fill distribution depends on the instantaneous depth of each pool.

Baldacci & Manziuk (2020) proposent un cadre Bayésien adaptatif où les paramètres du modèle (drift, intensité d'arrivée, profondeur) sont mis à jour en temps réel à partir des observations. Le contrôle stochastique est résolu par différences finies ou par deep RL selon la complexité ; les extensions naturelles incluent les signaux short/long, l'impact de marché et la liquidité cachée.Baldacci & Manziuk (2020) propose an adaptive Bayesian framework where model parameters (drift, arrival intensity, depth) are updated in real time from observations. The stochastic control problem is solved by finite differences or by deep reinforcement learning depending on complexity; natural extensions include short/long signals, market impact and hidden liquidity.

Combinaison opérationnelle: dans HFThot Quant nous combinons les deux approches — l'OU multi-actif fournit le squelette stratégique (panier, demi-vies, contrôle $v^\star$), et la couche Bayésienne Baldacci-Manziuk re-route en temps réel les ordres entre pools selon l'imbalance et le spread instantanés. Le moteur de routage est exposé via app/services/execution/cross_pool_router.py (tier Quant).Operational combination: in HFThot Quant we combine both approaches — the multi-asset OU provides the strategic skeleton (basket, half-lives, $v^\star$ control), and the Baldacci-Manziuk Bayesian layer routes orders in real time across pools based on instantaneous imbalance and spread. The router is exposed via app/services/execution/cross_pool_router.py (Quant tier).

9. Industrialisation dans HFThot ThotCloud LabIndustrialisation in HFThot ThotCloud Lab

Le solveur OU multi-actif est intégré dans la page Streamlit 🔬 Microstructure Lab (onglet 🎯 OU optimal execution) et sert le pipeline complet:The multi-asset OU solver is integrated in the Streamlit page 🔬 Microstructure Lab (tab 🎯 OU optimal execution) and powers the complete pipeline:

Multi-select de panier avec parsing CCXT natif (BTC/ETH/SOL/AVAX/...).Basket multi-select with native CCXT parsing (BTC/ETH/SOL/AVAX/...).

Échantillonneur historique persistant en session_state.Calibration history sampler persisted in session_state.

Demi-vies par actif affichées et éditables.Per-asset half-lives displayed and editable.

Dropdowns Objectif (Mean-variance / Min-variance / Max-PnL) et Horizon (5 min / 30 min / EOD / EOW / Custom).Objective dropdown (Mean-variance / Min-variance / Max-PnL) and Horizon dropdown (5 min / 30 min / EOD / EOW / Custom).

Inputs $\gamma$ et $\eta$ pour ajuster aversion au risque et impact.$\gamma$ and $\eta$ inputs for risk aversion and impact tuning.

Vecteur d'inventaire $q_0$ et nombre de trajectoires.Inventory vector $q_0$ and number of paths.

Plans HFThot et accès aux fonctionnalitésHFThot tiers & feature access

TierTier

PrixPrice

Solveur OU multi-actifOU multi-asset solver

Routeur cross-poolCross-pool router

Paper-tradingPaper-trading

GratuitFree

0 €€0

—

—

—

ÉducationEducation

9 €/mois€9/mo

—

—

✓ limité✓ limited

ProPro

49 €/mois€49/mo

—

—

✓

QuantQuant

199 €/mois€199/mo

✓ complet✓ full

✓ Bayésien✓ Bayesian

✓ illimité✓ unlimited

InstitutionnelInstitutional

sur demandecontact us

✓ + γ/η custom✓ + custom γ/η

✓ + venues custom✓ + custom venues

✓ multi-comptes✓ multi-account

10. Aller plus loin: cours prérequis & notebook approfondiGo deeper: prerequisites course & advanced notebook

Cet article suppose une familiarité avec le contrôle stochastique et le calcul d'Itô multidimensionnel. Pour les lecteurs souhaitant tout reconstruire à partir de zéro — du lemme d'Itô à la dérivation complète des EDOs Riccati matricielles, en passant par Hayashi-Yoshida et la valorisation rough-Heston — nous publions deux ressources commerciales complémentaires:This article assumes familiarity with stochastic control and multi-dimensional Itô calculus. For readers wishing to rebuild everything from scratch — from Itô's lemma to the full derivation of matrix Riccati ODEs, including Hayashi-Yoshida and rough-Heston pricing — we publish two complementary commercial resources:

Cours LaTeX + NotebookLaTeX course + Notebook

34,99 €

Achat unique, accès à vie · 78 pages. Cours LaTeX tcolorbox + TikZ + pgfplots, dérivation rigoureuse: lemme d'Itô multi-dim → HJB → ansatz quadratique → Riccati matriciel → preuve d'existence/unicité globale. Notebook compagnon Python avec preuves numériques de chaque étape.One-off purchase, lifetime access · 78 pages. LaTeX course tcolorbox + TikZ + pgfplots, rigorous derivation: multi-dim Itô lemma → HJB → quadratic ansatz → matrix Riccati → global existence/uniqueness proof. Companion Python notebook with numerical proofs at every step.

Achat unique · 15 pages PDF + notebook Jupyter. Le bagage mathématique minimum pour aborder le cours sereinement : équations de Riccati, contrôle stochastique, processus de Hawkes, solutions de viscosité, analyse convexe. Notebook avec exemples Itô résolus pas-à-pas.One-off · 15-page PDF + Jupyter notebook. The minimum mathematical baggage to read the main course comfortably: Riccati equations, stochastic control, Hawkes processes, viscosity solutions, convex analysis. Notebook with worked Itô examples step-by-step.

12 cellules KaTeX dans le notebook12 KaTeX cells in the notebook

📚 Aperçu gratuit : téléchargez le notebook prérequis (sample) — 3 cellules d'aperçu sur Itô multi-dim et l'ansatz quadratique. Pour le PDF complet (15 p.) et toutes les cellules résolues, voir le pack ci-dessus.📚 Free preview: download the prerequisites notebook sample — 3 preview cells covering multi-dim Itô and the quadratic ansatz. For the full PDF (15 p.) and every solved cell, grab the pack above.

11. RéférencesReferences

Bergault, P., Drissi, F. & Guéant, O. (2022). Multi-asset optimal execution and statistical arbitrage strategies under Ornstein-Uhlenbeck dynamics. SIAM Journal on Financial Mathematics, 13(1), 353–390.

Baldacci, B. & Manziuk, I. (2020). Adaptive trading strategies across liquidity pools. arXiv:2008.07807 [q-fin.TR].

Almgren, R. & Chriss, N. (2001). Optimal execution of portfolio transactions. Journal of Risk, 3(2), 5–40.

Avellaneda, M. & Stoikov, S. (2008). High-frequency trading in a limit order book. Quantitative Finance, 8(3), 217–224.

Hayashi, T. & Yoshida, N. (2005). On covariance estimation of non-synchronously observed diffusion processes. Bernoulli, 11(2), 359–379.

Cartea, Á., Jaimungal, S. & Penalva, J. (2015). Algorithmic and High-Frequency Trading. Cambridge University Press.

🎯 Lancez votre propre exécution OU multi-actif🎯 Run your own multi-asset OU execution

Solveur Riccati matriciel + Monte-Carlo + planning panier en un clic, sur LOB live, dans HFThot ThotCloud Lab.Matrix Riccati solver + Monte-Carlo + basket schedule in one click, on live LOB, inside HFThot ThotCloud Lab.